The Agricultural Development Bank of China (ADBC) has been pumping money into China's agricultural sector by financing most of the grain and cotton marketed this year and lending for poverty alleviation, land improvement, marketing infrastructure, agricultural industry parks, "leading enterprises," and agricultural science and technology. The bank is one more seldom-noticed example of a Chinese economy increasingly propped up by debt.

With downward pressure on many commodity prices, ADBC loans are holding up sagging crop markets. In a press conference last month, the bank's president touted ADBC's role in maintaining food security by announcing that ADBC lent 170.4 billion yuan ($24.3 billion) to finance purchases of 124 million metric tons of grain and oil in the first three quarters of 2019--up 87 percent from last year. The ADBC president acknowledged that the bank financed 75 percent of wheat sales this year and 71 percent of early rice purchases. These shares were up from 49 percent last year. The boom probably reflects the 31 million metric tons of wheat purchased through the minimum price program--the largest total since 2008. Early rice production was down sharply this summer as farmers cut back on double-cropping, but officials still had to support the price with purchases at the minimum price.

The fall grain harvest happens in the fourth quarter, and the bank has announced that it has 160 billion yuan ($22.8 billion) of "money waiting for grain" to finance procurement of this year's fall grain crop. That's slightly more than last year when the bank financed half of fall grain purchases. Five rice-growing provinces have already begun minimum-price purchases of their fall rice crops which news media credit for price rebounds. Minimum-price purchases of medium grain rice are expected to begin in northeastern provinces after an audit of warehouses is complete. Markets are watching carefully to see whether big rice provinces Hunan and Jiangxi launch the program.

There is no longer a formal price support for corn or soybeans, but ADBC finances purchases for government reserves when the market looks weak. There were rumors in October that the government was considering purchasing corn for reserves, but nothing concrete. Officials are probably monitoring downward pressure on corn prices to determine whether they need to intervene as more grain is sold by farmers and demand remains soft due to the decimated pig herd and weak starch production. Chinese soybean prices fell to their lowest point in 5 years last weekend, but China's grain reserve company swooped in to make additional purchases--almost certainly financed by ADBC--to spark a rebound in prices.

The Agricultural Development Bank of China (ADBC) was carved out of the Agricultural Bank of China (ABC) in a 1994 reform that created specialized banks to carry out government policies, thus freeing up ABC and other state-owned banks to focus on commercial-oriented lending. ADBC's primary function historically was to finance the marketing of grain, edible oils, and cotton by state-owned enterprises. (Other policy banks focus on financing infrastructure and foreign trade.) ADBC is financed mainly by selling bonds. ADBC is one of the top three bond-issuers in China with 4.45 trillion yuan in bonds outstanding.

ADBC's outstanding loan balance has been doubling every five years--from 1.2 trillion yuan in 2008 to 2.5 trillion yuan in 2013, and 5.1 trillion yuan at the end of 2018. The ratio of the loan balance to the total value-added of China's agriculture, forestry and fishing has more than doubled from about 35 percent in 2004 to 75 percent in 2018--an indicator that loans have grown at a faster pace than the agricultural sector.

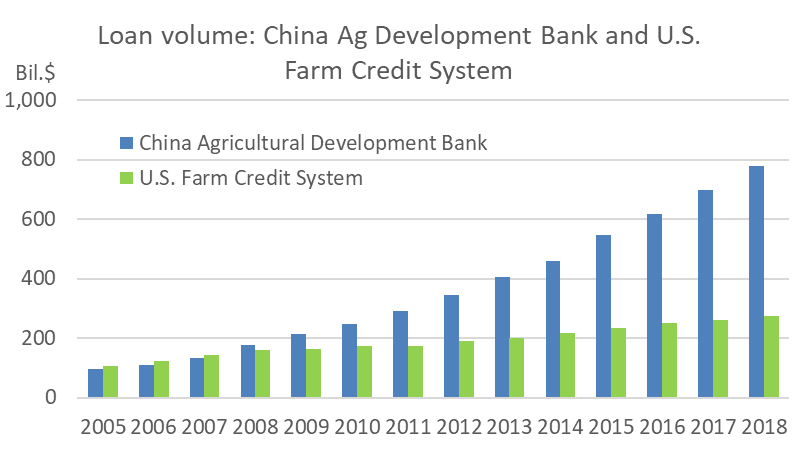

Here's another indicator of how ADBC's loan portfolio has grown. In 2005, ADBC's loan balance was about $10 billion less than the U.S. Farm Credit System's $106 billion. The ADBC loan balance surpassed that of FCS in 2008 and has continued soaring over the last decade. By 2018, ADBC's loan balance of $777 billion exceeded the FCS loan balance by 180 percent.

ADBC lends mainly to grain trading and processing enterprises to make sure farmers do not have difficulties selling grain or receive IOUs in payment--occurrences that were common in the 1990s. Grain, cotton and oilseed procurement accounted for the biggest chunk of ADBC's portfolio in 2018 with a loan balance of about $265 billion. Poverty alleviation loans are now a close second, with a loan balance of about $192 billion last year. A little less than half the anti-poverty loans are for infrastructure, and they also include lending earmarked to buy grain, oil and cotton in poor regions.

"Agricultural modernization" is the third chunk of loans described in the 2018 annual report, with a smaller balance of about $31 billion. These include loans for marketing system development ($6.5 billion), so-called "dragon head" agricultural business enterprises ($4.7 billion), high-standard farmland projects, support for agricultural industry parks and "protected zones" for key commodities, and agricultural S&T. ADBC has loans to support "new-style" scaled-up farms. ADBC recently announced intentions to lend 50 billion yuan to support hog production over the next three years. ADBC finances transportation of grain from north to south.

Historically, China's banking system has siphoned money out of the countryside via peasants making deposits in postal savings banks and credit cooperatives which then deposit the funds in city-based banks or real estate and industrial investments. ADBC is reversing that tide by sending some of that same money from bond-buyers (probably commercial banks) back to the countryside, but it would be more efficient to develop self-contained credit markets in the countryside. One of ADBC's current initiatives is to jump-start "marketized" lending in the countryside by capitalizing loan guarantee entities run by provincial governments intended to reduce risk of bank lending to private grain traders and processors.

In theory, ADBC's money pipeline to the countryside is one of the few mechanisms to reduce the massive inequality in China. But the system has built-in incentives for corruption--a lot of the money was stolen by corrupt officials and unscrupulous warehouse operators--and one wonders whether the lending is unsustainable. ADBC claims its non-performing loan ratio is only 0.4 percent but it seems unlikely that loans for moldy, poisoned or nonexistent grain, fields producing crops that are falling in price, and apartment complexes for elderly peasants can be paid back. Moreover, the ADBC reflects the Chinese communist tendency to rely on behemoths. ADBC is itself a behemoth and one of its stated strategies is to help other creations of central planners--COFCO, Sinograin, the Supply and Marketing Cooperatives, and a State investment company--to "play a leadership role in the market" and stabilize market expectations.

With downward pressure on many commodity prices, ADBC loans are holding up sagging crop markets. In a press conference last month, the bank's president touted ADBC's role in maintaining food security by announcing that ADBC lent 170.4 billion yuan ($24.3 billion) to finance purchases of 124 million metric tons of grain and oil in the first three quarters of 2019--up 87 percent from last year. The ADBC president acknowledged that the bank financed 75 percent of wheat sales this year and 71 percent of early rice purchases. These shares were up from 49 percent last year. The boom probably reflects the 31 million metric tons of wheat purchased through the minimum price program--the largest total since 2008. Early rice production was down sharply this summer as farmers cut back on double-cropping, but officials still had to support the price with purchases at the minimum price.

The fall grain harvest happens in the fourth quarter, and the bank has announced that it has 160 billion yuan ($22.8 billion) of "money waiting for grain" to finance procurement of this year's fall grain crop. That's slightly more than last year when the bank financed half of fall grain purchases. Five rice-growing provinces have already begun minimum-price purchases of their fall rice crops which news media credit for price rebounds. Minimum-price purchases of medium grain rice are expected to begin in northeastern provinces after an audit of warehouses is complete. Markets are watching carefully to see whether big rice provinces Hunan and Jiangxi launch the program.

There is no longer a formal price support for corn or soybeans, but ADBC finances purchases for government reserves when the market looks weak. There were rumors in October that the government was considering purchasing corn for reserves, but nothing concrete. Officials are probably monitoring downward pressure on corn prices to determine whether they need to intervene as more grain is sold by farmers and demand remains soft due to the decimated pig herd and weak starch production. Chinese soybean prices fell to their lowest point in 5 years last weekend, but China's grain reserve company swooped in to make additional purchases--almost certainly financed by ADBC--to spark a rebound in prices.

The Agricultural Development Bank of China (ADBC) was carved out of the Agricultural Bank of China (ABC) in a 1994 reform that created specialized banks to carry out government policies, thus freeing up ABC and other state-owned banks to focus on commercial-oriented lending. ADBC's primary function historically was to finance the marketing of grain, edible oils, and cotton by state-owned enterprises. (Other policy banks focus on financing infrastructure and foreign trade.) ADBC is financed mainly by selling bonds. ADBC is one of the top three bond-issuers in China with 4.45 trillion yuan in bonds outstanding.

ADBC's outstanding loan balance has been doubling every five years--from 1.2 trillion yuan in 2008 to 2.5 trillion yuan in 2013, and 5.1 trillion yuan at the end of 2018. The ratio of the loan balance to the total value-added of China's agriculture, forestry and fishing has more than doubled from about 35 percent in 2004 to 75 percent in 2018--an indicator that loans have grown at a faster pace than the agricultural sector.

|

| Source: ADBC annual reports and National Bureau of Statistics web site. |

|

| Source: Annual reports of Agricultural Development Bank of China and U.S. Farm Credit System. |

"Agricultural modernization" is the third chunk of loans described in the 2018 annual report, with a smaller balance of about $31 billion. These include loans for marketing system development ($6.5 billion), so-called "dragon head" agricultural business enterprises ($4.7 billion), high-standard farmland projects, support for agricultural industry parks and "protected zones" for key commodities, and agricultural S&T. ADBC has loans to support "new-style" scaled-up farms. ADBC recently announced intentions to lend 50 billion yuan to support hog production over the next three years. ADBC finances transportation of grain from north to south.

Historically, China's banking system has siphoned money out of the countryside via peasants making deposits in postal savings banks and credit cooperatives which then deposit the funds in city-based banks or real estate and industrial investments. ADBC is reversing that tide by sending some of that same money from bond-buyers (probably commercial banks) back to the countryside, but it would be more efficient to develop self-contained credit markets in the countryside. One of ADBC's current initiatives is to jump-start "marketized" lending in the countryside by capitalizing loan guarantee entities run by provincial governments intended to reduce risk of bank lending to private grain traders and processors.

In theory, ADBC's money pipeline to the countryside is one of the few mechanisms to reduce the massive inequality in China. But the system has built-in incentives for corruption--a lot of the money was stolen by corrupt officials and unscrupulous warehouse operators--and one wonders whether the lending is unsustainable. ADBC claims its non-performing loan ratio is only 0.4 percent but it seems unlikely that loans for moldy, poisoned or nonexistent grain, fields producing crops that are falling in price, and apartment complexes for elderly peasants can be paid back. Moreover, the ADBC reflects the Chinese communist tendency to rely on behemoths. ADBC is itself a behemoth and one of its stated strategies is to help other creations of central planners--COFCO, Sinograin, the Supply and Marketing Cooperatives, and a State investment company--to "play a leadership role in the market" and stabilize market expectations.

Comments

Inequality has been dropping like a rock since Xi made Gini improvement a requirement for official promotions in 2012. Today its 38.5 compared to America's 41.5, and that doesn't account for the fact that all poor Chinese own their homes free and clear.

China’s rural, inland people have always been poorer than their urban, coastal cousins and, because the country couldn’t afford to build homes and cities fast enough, inlanders have been held in place by residential hukous. But economists[1] have discovered that their inequality was exaggerated. The cost of living in Shanghai and Shenzhen is much higher because land prices and basic food costs are much higher. Housing quality is the same in both regions and basic food costs in rural areas are half Beijing’s. Researchers analyzed the full range of goods and services and concluded that incomes from rural areas should be increased by fifty percent to make them comparable.

Then, when they adjusted for where people actually live the difference shrank further. Until recently, demographers counted people’s hukous–where they were registered to live–rather than where they actually lived. As migrant workers’ numbers rose to three hundred million in 2018, their movement severely distorted the statistics. In real life, the coastal provinces have millions more residents than their registered populations and the migrant-sending inland provinces have millions less. When someone moved from the interior to the coast, they lifted inequality indicators because she contributed to income in the coastal destination but was still counted as living in her rural home. Once they corrected[2] this counting error, analysts found that regional inequality has declined by forty-two percent since 1978, at 1.1 percent annually. In 2002, fourteen Guizhou workers earned as much as the average[3] Shanghainese, but by 2019, it took only five. Nor was the structural gap as painful as it sounds. Across the country, everyone saw everyone else they could see getting richer each year and, to rural villagers buying their first pickup truck, Shanghai’s glitzy lifestyle was no more relevant than New York’s.