News media have been reporting tentative agreements between China and Ukraine in which the Ukraine would export corn to China and China would make investments in Ukraine. In early December, Xinhua announced that an agreement had been signed with COFCO to buy Ukrainian corn, but several days later an official from a Ukrainian agribusiness company announced that "in principle" Ukrainian corn could enter China, but there seemed to be a hang-up on which Chinese company owned the import quota that would allow them to buy it.

At least two meetings on agricultural investment were held during a Ukrainian agribusiness official's December visit to Beijing. One meeting held by the Chinese Animal Agriculture Association was convened specifically to discuss investment opportunities in Ukraine. A second meeting of Chinese business leaders on agricultural investment--both in China and overseas--was sponsored by a business magazine and included the Ukrainian official as well as Chinese economists and business leaders.

News media reports on these two proceedings indicate that Chinese government and business leaders acknowledge that Chinese farms cannot supply the growing need for agricultural products--corn, in particular--and business investment is needed to upgrade production capacity. However, business investment in Chinese agriculture is hamstrung by the need to keep peasants tied to their land. Therefore, Chinese companies are being encouraged to invest in building industrialized farms overseas in places like the Ukraine, one of the most fertile regions in the world which has a collection of deteriorating Soviet-era farms badly in need of investment. However, Chinese companies have discovered that other countries also are suspicious of business investment in agriculture and are proceeding with caution in their investment plans.

The livestock association meeting featured an American consultant engaged to facilitate investment in Ukraine. There has been a government-to-government agreement on Chinese imports and investment, and China's Import-Export Bank has pledged $3 billion in financial backing for the project. A Ukrainian company registered in the U.S. with investment from big players like Goldman Sachs, JP Morgan Chase and the Kuwait investment authority is also involved. This meeting apparently was held to recruit Chinese companies to engage in concrete investment projects in the Ukraine.

The meeting participants were told that the Ukraine has 33 million hectares of black soil and abundant water resources. They were told Ukraine's annual grain consumption is about 30 million metric tons and its production capacity is 100 mmt or more, so there is great potential for Ukrainian grain exports. The Ukraine has many moribund former collective farms from the Soviet era with backward infrastructure desperately in need of investment in equipment, grain storage and other infrastructure. Chinese investors were told Ukrainian land rents are in the range of $35-$90 per hectare (2.5 acres). Rental agreements are for 15 years and can be renewed three times for a total of 60 years.

Chinese officials said the Ukrainian investment project is expected to help supply China's grain needs and provide opportunities to score financial gains as well. Chinese livestock association officials at the meeting expressed interest but were noncommittal. They promised to evaluate possible projects, recruit potential Chinese investors and go on a fact-finding tour of the Ukraine. They noted that investment projects should be focused on crop and livestock farming and called for careful consideration of projects, including the government's attitude and regulations. There was a brief discussion of political stability in the Ukraine. (see this post on problems encountered in China's overseas investment in agriculture.)

The business leaders' meeting was a more general discussion with the theme, "cool thinking on hot investment in agriculture." The Chairman of a Ukrainian agribusiness company was the first speaker, but the speakers also included representatives from several Chinese companies and two economists from government think tanks. In brief remarks, the Ukrainian official made a general pitch for Chinese investment to promote Ukrainian grain exports to China. Speakers observed that China's booming imports of soybeans and even rice, wheat and corn showed that China's resources are not sufficient to keep the country self-sufficient. The meeting's moderator noted that Ukrainian corn was 40-percent cheaper than U.S. corn and asserted that opening more import channels was a way to improve China's future food security.

Why are Chinese companies are being encouraged (and subsidized with loans from state-owned banks) to invest in Ukrainian farmland, rather than investing in Chinese farmland? One reason is that Ukrainian land is a lot cheaper. The rents of $35-$90 per hectare are much cheaper than Chinese rents of 300-to-500 yuan per mu which work out to about $700-$1200 per hectare. The 15-year Ukrainian rental agreements are more secure than Chinese short-term agreements that undermine incentives to make long-term investments (see this post). However, at the root of the push to invest overseas is the fact that Chinese farmland has lots of people living on it.

Authorities have decided to place strict limits on acquisition of Chinese farmland by business enterprises. At the business leaders meeting, an economist from the State Council's Development Research Center (DRC) noted the special nature of agriculture that sets it apart from other types of investment. Hu Jintao declared that agriculture is a foundational industry for tranquility, support of the people and national self-reliance. It has so-called "externalities" associated with maintaining food security and it serves as a reservoir of labor for industrial development, explained the DRC economist.

During the question and answer period, the owner of a construction company asked whether the government would endorse moving farmers into high rise apartments in newly-built rural towns, thus freeing up land for large-scale farms operated by companies. In response, an economist from a Ministry of Agriculture think tank replied, "You have raised a very strong policy-oriented issue." The economist said the people are "tied" to the land, so if a company rents their land, "what will they do?" The government views farmland as a means of guaranteeing minimum subsistence for the peasants and a fall-back if they lose their factory jobs. He gave the current party line: the government does not encourage companies to engage in long-term or large-scale rentals of Chinese farmland, but it does encourage companies to invest in rural infrastructure and to provide services to farmers. The discussion also included rhetoric about how Chinese companies need to invest in agriculture as a social responsibility with a long-term payoff (implying that they shouldn't expect to make any profits in the short or medium term).

The contrast between China and Ukraine in farmland today goes back to the different approaches to agriculture followed by the Soviets and Chinese during the 20th century. The Soviet Union formed massive collective farms and starved or shot the peasants if they raised objections. China briefly tried to follow that model in the late 1950s with disastrous consequences, but they never went as far as the Soviets, and Chinese farm communes were organized around traditional villages. The Chinese were able to return to a family farming model in the late 1970s after the commune model of agriculture had clearly failed. Under the "household responsibility system" installed during 1978-83, collective "ownership" of land by village families was maintained, but the rights to cultivate the land and derive benefits from it were distributed to families who were members of village collectives.

The Soviets cleared most of the Ukrainian peasants off the land several generations ago, leaving big tracts of land corporate-farming-ready. In contrast, China's farmland is still occupied by a massive population of peasants who don't directly own their land but are tied to it through their collective "ownership." The MOA economist said "our people are tied [to the land]." The Chinese word translated "tied" is "结合" which can mean "combine," "linked," or "united in wedlock." In other words, Chinese peasants are combined with their land like medieval European serfs who occupied and cultivated land that was owned by the lord of the manor in exchange for the lord's protection. Chinese peasants are, in effect, vassals of the communist party leaders who are the de facto "owners" of land who can sell it and reap capital gains. To their credit, the Chinese communist party has eliminated the explicitly feudalistic requirements to deliver grain to the State, pay agricultural taxes and corvee labor requirements. However, Chinese "collective" land ownership still retains the vestiges of a feudal system that officials are trying to undo. Ironically, the Ukraine was considered one of the main centers of serfdom in Europe. The Soviets took over the land from the manorial lords and their Ukrainian technocrat descendants are now preparing to rent it out to Chinese companies.

The second measure that defines the Chinese neo-feudal system and keeps peasants on the land is the household registration system which prevents rural residents from becoming legal residents of cities. The wikipedia entry on serfdom notes that "[serfs] were tied to the land and could not move away without their lord's consent and the acceptance of the lord to whose manor they proposed to migrate to." This sounds identical to China's household registration system.

The Ministry of Agriculture economist's reply to the question about developing rural land zeroes in on land issues Chinese officials are grappling with. He told the Hebei construction company official that developing rural land involves some thorny issues that need more "research." For example, he says, if you consolidate a parcel of rural land and then develop it, how is the increased value of the land distributed? What proportion of the increased value do the peasants get? (The normal practice has been to compensate peasant "owners" only for the value of grain that the land could produce--a miniscule amount. Most of the value of newly-developed rural land goes to officials, local government coffers or business enterprises.) Officials are preparing to announce some new guidelines or regulations that will require that peasants be given a higher proportion of the capital gain on land developed for nonfarm use.

Chinese Chickens on Drugs

On December 18, China's central television network (CCTV) revealed that some farms use as many as 20 different drugs to raise chickens, and some use excessive doses or banned drugs. This incident again shines a light on pervasive food safety problems in China as the country adopts an industrialized food system. Laws, regulations, and certifications present on paper are routinely flouted and there is seemingly no effective mechanism that can assure final consumers that their food is safe to eat.

The main revelation of the CCTV report was that farms in several locations of Shandong Province violated regulations that require farms to stop feeding drugs to chickens 7 days prior to slaughter. The chickens were delivered to local slaughterhouses of big poultry meat companies, Liuhe and Wintech, which supplied fast food chains like KFC and McDonalds.

The main revelation of the CCTV report was that farms in several locations of Shandong Province violated regulations that require farms to stop feeding drugs to chickens 7 days prior to slaughter. The chickens were delivered to local slaughterhouses of big poultry meat companies, Liuhe and Wintech, which supplied fast food chains like KFC and McDonalds.

A cartoon from a Chinese commentary mocking the use of drugs for raising chicken: "Chicken 'famine'"

The farms raised "white feathered" chicken breeds known in China as "quick chickens" (速生鸡) because they grow to a market weight of about 5 lbs in 40 days. In comparison, native breed "yellow-feathered" chickens take 100 days to reach about 2 lbs. and traditional free range chickens are raised for a year. According to a news media report, the "quick chickens" are raised in houses 15 x 50 meters containing thousands of birds--15 chickens per square meter according to one farmer's estimate. The lights are left on night and day to encourage the birds to eat as much as possible. The boss of one Shandong chicken farm says the stress and the failure of birds' internal organs to keep up the growth of their bodies leaves them in a weakened state and vulnerable to illness. The farm operator insists that following the regulations would kill the birds since they can't survive more than 3-to-5 days without drugs.

According to reports, Shandong farms give chickens as many as 20 different pharmaceuticals. One company farm boss said they alternate two antibiotics--amoxicillin and chloromycetin--to prevent pathogens from developing resistance. Regulations forbid use of ofloxacin--a drug often used to treat human ear infections--within 28 days of slaughter, but many farms use it up to 2 days before slaughter.

One of the strategies adopted by the farmers is to give the birds a steriod called dexamethasone that promotes weight gain and speeds up the production cycle to 35 days.

Another cartoon--but the "quick chicken" is shown with yellow feathers

instead of white feathers that "quick chickens" are known for

The focus of the CCTV report was on two antiviral drugs, ribavrin and amantadine, which have been banned for use in poultry since 2005. Amantadine was introduced in the during the 1960s to treat Asian flu in humans. According to a 2005 Washington Post article, Chinese farmers began using amantadine to treat chickens for avian influenza in the 1990s, and government veterinarians promoted its use during China's big AI epidemic in 2004-05. Widespread use of amantadine is blamed for developing resistance in the H5N1 strains of the virus in China, Thailand and Vietnam that rendered the drug useless for treating humans.

Chinese regulations require chicken farms to keep detailed records on daily use of medications, chickens' health status, the sale date and purchases of inputs. According to the news media report, the farm records were filled out by inspectors at the slaughterhouse. Inspectors at slaughterhouses said animal quarantine certificates were issued even though the chickens were never tested.

Some of the Chinese news media reports focus on the culpability of Yum Brands, the company that operates KFC restaurants in China. The Liuhe slaughterhouse in Shandong had supplied chicken to Yum for use in its fast food restaurants in Shanghai, hundreds of miles from Shandong. Yum paid a laboratory operated by the Shanghai Municipal Food and Drug Administration to test samples of the meat supplied by Liuhe every two months. Although the lab is under the Shanghai FDA, this testing was not part of its government food safety monitoring function--such labs often act as a quasi-private-sector "third-party" testing entity on a fee basis for private businesses.

According to another news media report, Yum had 19 batches of chicken tested by the Shanghai lab during 2010-11, and 8 of those batches tested positive for excessive antibiotic residues. There were no tests for hormones.

Yum acknowledged that tests revealed excessive drug residues in some chicken supplied by Liuhe in 2010. Yum cut off a Liuhe supplier in Shandong's Linyi county in 2011 and journalists discovered a farm there that had been closed down for about a year. On December 18, 2012 the Yum company issued a statement saying that it had stopped procuring chicken from Liuhe in August of this year, initially with a vague explanation that it was for reasons of "survival of the fittest" without citing drug problems. A Yum official later said that the company had ceased its supplier relationship with Liuhe for multiple reasons that included the company's service, price and business direction. The 21st Century Business Herald accuses Yum of concealing the test results from the public and failing to issue any recalls.

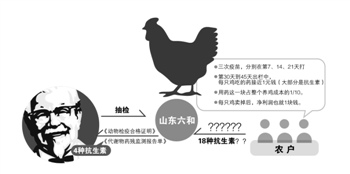

This graphic accompanied an article reporting on the problems with testing chickens for pharmaceuticals. "Farmers" on the right use "18 kinds of antibiotics" on chickens before selling them to the Shandong Liuhe slaughterhouse (gray circle in the center). Yum Brands (represented by the Colonel Sanders logo) tests for "4 kinds of antibiotics."

This week the Shanghai Food Safety Commission sent out its inspectors to gather samples of chicken from Yum's distribution centers in Shanghai. Out of 8 batches tested for 29 kinds of antibiotics, hormones and antiviral drugs, they found only one sample that tested positive for amantadine. The tests were done at the same testing center that did the testing commissioned by Yum in the past.

In Shandong, the livestock bureau and police organized teams to inspect chicken farms. Two guilty farms have been shut down. Farm operators were detained in one district and hauled in for questioning in another. Two slaughter houses operated by Liuhe and Wintech have been shut down for rectification and raw materials seized for testing and inspection.

This incident has some similarities to the pork industry's clenbuterol ("lean meat powder") incident revealed in March 2011.

- Both incidents were revealed by CCTV reports.

- Both incidents involved illegal use of drugs by farms that supplied local subsidiaries of major meat companies.

- Farms in both incidents had adopted U.S.-style production systems that utilize animals bred to grow to maturity rapidly in a tightly-controlled environment.

- In both incidents required testing was either ignored or falsified and purveyors of the meat in far-off cities either were oblivious to the practice or covered it up.

The incident raises the question of how safety assurances can be built into supply chains when consumers and producers are separated by hundreds of miles and multiple companies. In theory, big agribusiness companies are supposed to function as "dragon heads" who give farmers training, technical information and help with adopting food safety measures. In reality, profit margins are razor-thin and the threat of disease is always looming. Companies, farmers and even inspectors have a similar interest in churning out animals. There is still an entrenched "the mountains are high and the emperor is far away" mentality in which you carry on business as usual in your locality, falsify records, and clean things up when provincial officials of auditors from the supermarket or restaurant chain come around for an inspection. Regulations, standards, and certificates exist on paper but the consumer can't have much confidence in these if they are routinely flouted.

The companies involved in this incident are parts of large companies that have an interest in avoiding food safety incidents. One suspicious facet of the incident is the focus of blame on Yum Brands, a theme also picked up by Stan Abrams' China Hearsay blog. The anti-KFC rhetoric is coming mainly from state-owned media outlets. Liuhe and its parent company, the feed giant New Hope Group, have direct responsibility for the incident but aren't getting much heat from the media. Liuhe supplies chicken to other customers and supermarkets. Some Beijing supermarkets are removing chicken products from the Liuhe company from their shelves, but this didn't get as much publicity as the role of Yum. Interestingly, there have been a couple of articles in the international media recently about KFC and McDonalds having a harder time competing with domestic Chinese fast food chains. Is there a behind-the-scenes nationalist campaign displace KFC from their leading position in China's fast food market?

One commentary in the financial news media noted that the stock prices of the companies involved were hit by the incident and it exacerbates a year-long slump in the broiler industry. The commentator speculated that a completely integrated supply chain in which the processor operates its own farms may be the most tightly-controlled and "safe" model, but argued that the "company + farmer" model is better suited to conditions in China and notes that this model is also used in developed countries. The commentary insisted that "company + farmer" is the model for the long term and must be combined with effective food safety laws and strict monitoring.

Ironically, a news media account in February this year praised the Liuhe company's innovative "chicken guarantee" model in Pingdu--one of the regions where drug use was discovered. Over 2,500 farmers got loans to buy chicks and feed that were paid back 45 days later when the chickens were sold to the company. Farmers supposedly would be paid the market price if chicken prices went up, but if the price went down before slaughter they would be paid a price that would cover their production costs. Farmers also got insurance, technical advice, and a guarantee that chickens would have a mortality rate of less than 5 percent. New Hope Group, Liuhe's parent company has similar arrangements for pig farmers in Sichuan. Once again, a seemingly carefully-thought-out "solution" has failed to prevent food safety problems.

A 2008 book by Warren K. Liu, KFC in China: Secret Recipe for Success, tries to explain why it's so hard to trust suppliers. Liu was a YUM brands executive in China during the 1990s. He only gave passing references to chicken farms on a few pages of his book but notes that he forced himself to visit countless farms and slaughterhouses. During his tenure KFC centralized and consolidated its supplier base, introduced a competitive bidding system, and took suppliers on tour of U.S. chicken farms. One of Liu's peeves was corruption which took up 6 pages of his chapter on supply chains. Despite strict rules on not accepting any gifts or entertainment and other measures to prevent corruption, Mr. Liu had to fire two employees who took kickbacks from suppliers. Liu agonized over the failure to completely root out corruption but finally concluded there was no way he could have prevented it. The tendency toward "local fiefdoms" in which suppliers, buyers and local officials build loyalty to one another is deeply entrenched in Chinese culture. It's not just a government problem; it's a business problem as well. Be careful whom you trust.

Socialism Needs a Private Sector?

According to the China's communist party leaders, private business needs to be able compete with state-owned businesses on equal footing in order to follow the road to socialism with Chinese characteristics.

On November 8, General Secretary Hu Jintao gave a typically long rambling "report" to the 18th party congress of the communist party which noted that China is still in an early stage of socialism and is now entering a new era of urbanization, industrialization, informationization, and modern agriculture. Secretary Hu observed that China faces many opportunities and challenges during this period when the world, China, and the party are encountering fundamental changes in conditions. He worried that China's development is still unbalanced, uncoordinated, unsustainable. Among the problems he cited were weak innovation capabilities, irrational industry structure, a weak foundation for agriculture, and food safety problems. He scolded some cadres for lacking ideals, forgetting their purpose and engaging in corruption.

Over the past couple of months Chinese officialdom has been busy studying the great spirit of the 18th party congress. One article, "China's Great Economic Transformation," describes the concepts at the core of the the new economic growth strategy which sounds like Chinese socialism with World Bank characteristics, as the concepts seem to be drawn from the World Bank-Development Research Center report issued earlier this year. While the World Bank describes the report as recommending steps toward a market economy, communist officials describe it as another stage in the journey toward socialism.

The transformation calls for innovation-driven development. This entails a transition from growth based on government investment and "extensive growth" based on exploiting factors of production to internally-generated growth based on innovation, upgrading technology and human resources.

The new strategy emphasizes fair and open competition. The "Great Transformation" article says a core problem of economic reform is giving privately-owned businesses equal access to factors of production, fair competition in markets, and equal protection under the law. This is described as a great innovation of "socialism with Chinese characteristics."

The author of this article traces the progression back to the third plenum of the 11th party congress in 1978 when it was proclaimed that some need to get rich first. In 1982 the 12th congress decided that nonpublic ownership is necessary and has man benefits. In 1992 it was proclaimed that a diversified economy is a long-term component of development and in 1997 non-public-ownership was declared to be an important part of the economy.

During Hu's reign at the top of China's communist party in 2002 began with an objective of "shoring up" the publicly-owned economy while encouraging and supporting the private sector. This followed several years of brutal reform and downsizing of the state-owned sector that began in the late 1990s. State-owned companies got access to bank loans, stock market listings, land, subsidies, and monopolies in some industries, prompting the "state comes in, private leaves" slogan in recent years.

The equal access strategy calls for breaking monopolies and lowing barriers to entry for private companies. It calls for a multi-level financial system that would presumably include another tier of banks that would lend to the private sector beneath the state-owned banks. The private sector should get equal access to resources and capital, says the "Great Transformation" article. It says the government should clarify its responsibilities and return to its original purpose. This seems to mean the government should become an impartial regulator, not a participant in business or a picker of winners.

This strategy will be hard to implement since the government has been busy giving state-owned companies a leg-up in many sectors. Agriculture and food sectors lack the real behemoths that dominate telecommunications, steel, railroads and banking. The feed and meat industries have a number of big private companies that got their start in the 1980s and '90s. However, the government has been busy trying to create big state-owned industry champions from the rump of the state grain-trading entities that originated during the central planning period. One reason for supporting these companies is to prevent domination of grain-trading, vegetable oil processing, seed breeding, and other industries by multinational companies. The handouts the state-owned companies get, including guaranteed loans from state-owned banks and help listing on Chinese or foreign stock markets, give state-owned companies guaranteed cash flow while private companies and farms have to start from nothing and compete against these behemoths.

Owners of monopolies have a strong interest in maintaining and strengthening their monopolies and other licenses to make easy money. For example, China has set aside a certain portion of tariff rate quotas to import several major commodities for state-owned enterprises. Ninety percent of the quota for wheat imports is reserved for state-owned companies. The other 10 percent is divided up among hundreds of applicants while one or two companies get the state-owned portion. That means if you want to import wheat you have to buy it from a state-owned company. These quotas are now becoming valuable as Chinese commodity prices move above world prices. The import quota system ultimately is a handout to COFCO and Sinograin. Are they going to give this up?

"Corporations" established to manage grain reserves get subsidies to buy and hold grain bought under price support programs. The government established a policy of raising prices every year which conveniently eliminates all downside risk of holding commodities. News media say that the grain reserve corporations make all their money from subsidies for holding reserves. They have little interest in making money from grain trading like private companies do.

Access to land is another handout to state-owned companies. On paper, rural land is owned by "collectives" which means no one really has concrete rights to it. The communist party rulers become the de facto owners and can expropriate it and sell it to a company (that party leaders likely have a financial interest in) at a low price at will. The company is happy to develop cheap land, sell it or borrow against it and pay taxes to the local government as a kickback. Who is going to break up this arrangement?

Funneling money to state-owned companies has been an integral part of the government's strategy to address problems like lack of innovation, food safety, and lack of infrastructure highlighted in the 18th party congress's plan.

What companies can afford "innovation", i.e. to hire PhDs, do R&D, buy expensive equipment, take trips abroad and attract overseas investors? Big state-owned companies.

In July agricultural officials convened a "modern agriculture" meeting in Heilongjiang where the China Development Bank pledged to shower cash on state-owned farms in that province to help them buy big tractors, airplanes to spray pesticides, and fancy irrigation systems.

In many industries, strategic plans call for raising the threshold for entering the industry. That means keeping out under-capitalized companies or shutting down companies that lack food safety testing capabilities, up-to-date facilities, and expensive certifications. The well-capitalized state-owned companies are left standing. About half of dairy processors were shut down last year in a re-licensing campaign and there are plans to consolidate industries like pork processing and seed breeding.

On November 8, General Secretary Hu Jintao gave a typically long rambling "report" to the 18th party congress of the communist party which noted that China is still in an early stage of socialism and is now entering a new era of urbanization, industrialization, informationization, and modern agriculture. Secretary Hu observed that China faces many opportunities and challenges during this period when the world, China, and the party are encountering fundamental changes in conditions. He worried that China's development is still unbalanced, uncoordinated, unsustainable. Among the problems he cited were weak innovation capabilities, irrational industry structure, a weak foundation for agriculture, and food safety problems. He scolded some cadres for lacking ideals, forgetting their purpose and engaging in corruption.

Over the past couple of months Chinese officialdom has been busy studying the great spirit of the 18th party congress. One article, "China's Great Economic Transformation," describes the concepts at the core of the the new economic growth strategy which sounds like Chinese socialism with World Bank characteristics, as the concepts seem to be drawn from the World Bank-Development Research Center report issued earlier this year. While the World Bank describes the report as recommending steps toward a market economy, communist officials describe it as another stage in the journey toward socialism.

The transformation calls for innovation-driven development. This entails a transition from growth based on government investment and "extensive growth" based on exploiting factors of production to internally-generated growth based on innovation, upgrading technology and human resources.

The new strategy emphasizes fair and open competition. The "Great Transformation" article says a core problem of economic reform is giving privately-owned businesses equal access to factors of production, fair competition in markets, and equal protection under the law. This is described as a great innovation of "socialism with Chinese characteristics."

The author of this article traces the progression back to the third plenum of the 11th party congress in 1978 when it was proclaimed that some need to get rich first. In 1982 the 12th congress decided that nonpublic ownership is necessary and has man benefits. In 1992 it was proclaimed that a diversified economy is a long-term component of development and in 1997 non-public-ownership was declared to be an important part of the economy.

During Hu's reign at the top of China's communist party in 2002 began with an objective of "shoring up" the publicly-owned economy while encouraging and supporting the private sector. This followed several years of brutal reform and downsizing of the state-owned sector that began in the late 1990s. State-owned companies got access to bank loans, stock market listings, land, subsidies, and monopolies in some industries, prompting the "state comes in, private leaves" slogan in recent years.

The equal access strategy calls for breaking monopolies and lowing barriers to entry for private companies. It calls for a multi-level financial system that would presumably include another tier of banks that would lend to the private sector beneath the state-owned banks. The private sector should get equal access to resources and capital, says the "Great Transformation" article. It says the government should clarify its responsibilities and return to its original purpose. This seems to mean the government should become an impartial regulator, not a participant in business or a picker of winners.

This strategy will be hard to implement since the government has been busy giving state-owned companies a leg-up in many sectors. Agriculture and food sectors lack the real behemoths that dominate telecommunications, steel, railroads and banking. The feed and meat industries have a number of big private companies that got their start in the 1980s and '90s. However, the government has been busy trying to create big state-owned industry champions from the rump of the state grain-trading entities that originated during the central planning period. One reason for supporting these companies is to prevent domination of grain-trading, vegetable oil processing, seed breeding, and other industries by multinational companies. The handouts the state-owned companies get, including guaranteed loans from state-owned banks and help listing on Chinese or foreign stock markets, give state-owned companies guaranteed cash flow while private companies and farms have to start from nothing and compete against these behemoths.

Owners of monopolies have a strong interest in maintaining and strengthening their monopolies and other licenses to make easy money. For example, China has set aside a certain portion of tariff rate quotas to import several major commodities for state-owned enterprises. Ninety percent of the quota for wheat imports is reserved for state-owned companies. The other 10 percent is divided up among hundreds of applicants while one or two companies get the state-owned portion. That means if you want to import wheat you have to buy it from a state-owned company. These quotas are now becoming valuable as Chinese commodity prices move above world prices. The import quota system ultimately is a handout to COFCO and Sinograin. Are they going to give this up?

"Corporations" established to manage grain reserves get subsidies to buy and hold grain bought under price support programs. The government established a policy of raising prices every year which conveniently eliminates all downside risk of holding commodities. News media say that the grain reserve corporations make all their money from subsidies for holding reserves. They have little interest in making money from grain trading like private companies do.

Access to land is another handout to state-owned companies. On paper, rural land is owned by "collectives" which means no one really has concrete rights to it. The communist party rulers become the de facto owners and can expropriate it and sell it to a company (that party leaders likely have a financial interest in) at a low price at will. The company is happy to develop cheap land, sell it or borrow against it and pay taxes to the local government as a kickback. Who is going to break up this arrangement?

Funneling money to state-owned companies has been an integral part of the government's strategy to address problems like lack of innovation, food safety, and lack of infrastructure highlighted in the 18th party congress's plan.

What companies can afford "innovation", i.e. to hire PhDs, do R&D, buy expensive equipment, take trips abroad and attract overseas investors? Big state-owned companies.

In July agricultural officials convened a "modern agriculture" meeting in Heilongjiang where the China Development Bank pledged to shower cash on state-owned farms in that province to help them buy big tractors, airplanes to spray pesticides, and fancy irrigation systems.

In many industries, strategic plans call for raising the threshold for entering the industry. That means keeping out under-capitalized companies or shutting down companies that lack food safety testing capabilities, up-to-date facilities, and expensive certifications. The well-capitalized state-owned companies are left standing. About half of dairy processors were shut down last year in a re-licensing campaign and there are plans to consolidate industries like pork processing and seed breeding.

China's Cotton Mountain Grows

China is creating a huge stockpile of cotton similar to the infamous "butter mountain" accumulated in the European Union during 1980s and earlier decades. Like the EU and U.S. during the 1980s and earlier, China has a minimum price for cotton that exceeds the market price. That means the government has to buy cotton to maintain the minimum price because private sector businesses can't make a profit buying cotton above the market price.

Unlike the E.U. and U.S. price support regimes of earlier decades, China has committed to relatively low tariffs and China is a net importer of cotton. The E.U. and U.S. subsidized exports of their commodity mountains, distorting world markets and leading to the adoption of disciplines on domestic support in the Uruguay Round of GATT. China, however, is accumulating a mountain of domestic cotton AND importing huge quantities of cotton. This is the perverse three-tier market described on this blog in October.

As of December 5, China's national cotton reserve corporation had purchased a cumulative 3.6 million metric tons of cotton from the 2012 harvest. This is the second year of massive stockpiling after the price support policy was introduced in 2011. The addition to the stockpile from this harvest so far exceeds the addition to last year's stockpile of about 3.1 mmt. Total reserves are now near 7.5 million metric tons. This exceeds China's annual production--estimated at 6.6 mmt this year--and is about 75 percent of USDA's estimate of China's annual consumption of cotton.

The cotton mountain phenomenon is exacerbated by weak demand for cotton from the Chinese textile industry. The textile business in China is still relatively slow. There are signs of recovery in domestic apparel sales but the export business is not good. Many companies report very slow orders.

For the most part, the only buyers of cotton in the China market now are companies that are authorized to buy at the minimum price. Private-sector operators are only buying cotton as they need it. Many companies in the textile business have either idled their factories or are running at a fraction of capacity. Those still operating are losing money and continue operating either to keep workers busy or to fulfill orders for high-end products. Inventories of unsold textiles are up. Companies are reportedly facing cash flow pressure. They have to repay outstanding loans before getting new ones. Many are having trouble paying their employees. Reportedly, more textile operators will have to shut down around the new year.

Imported cotton is cheaper than domestic cotton at the support price, so companies looking for cotton try to get imports. Cotton imports are controlled by a tariff rate quota system installed after WTO accession. According to a cotton industry report, quotas to import have become a valuable right. Some trading companies holding quotas import cheap cotton and resell it to Chinese companies at a price near the support price. Some textile industry people say the availability of cotton imported at the 40 percent sliding scale tariff has recently been restricted by some unspecified policies.

China's imports of cotton soared to 5.4 mmt during 2011/12, more than double imports of about 2.5 mmt during the previous two years. According to Chinese customs statistics, imports during the first two months of the 2012/13 market year are at about the same pace as last year.

Why did China pursue this policy? According to Ministry of Agriculture surveys, farmers wanted a price support policy. Ministry economists explained in a 2011 report that the policy was meant to address "cobweb"-type oscillations in the cotton market--a low price induces a decline in production which leads to high prices the following year, which leads to expanding production, which leads to low prices... Previously, the government tried to manage reserves to stabilize the cotton market, but it didn't have much impact and farmers didn't perceive any benefit from the policy.

An unspoken strategy behind the cotton policy is to buy regional stability in China's restive northwest Xinjiang "autonomous" region. Chinese authorities built up a cotton industry in Xinjiang during the 1990s to maintain self-sufficiency as cotton use swelled and eastern production areas faced pest problems. Xinjiang now accounts for nearly half of China's cotton production and would be one of the top producers in the world if it were a country. About two-thirds of the reserve purchases under the price support program are made in Xinjiang.

Xinjiang borders several central Asian countries and was the site of violent protests by the native Uighur population in 2009 and 2011. China's President Hu Jintao recently noted that policies are tilted toward border regions (check) and ethnic minority regions (check). A Ministry of Agriculture article offering recommendations for the design of the policy noted the importance of supporting poor farmers in Xinjiang who, unlike farmers in eastern China, had no good alternatives to growing cotton.

The problem with creating a cotton industry in Xinjiang is that it's thousands of miles from the textile industry and there has been very little progress in developing a local industry beyond basic cotton-ginning and trading. On December 7, a team of officials from the National Development and Reform Commission, Railway Ministry, Supply and Market Cooperative and National Cotton Reserve Corporation went to Xinjiang to inspect the situation regarding purchase, reserves and transportation of cotton. This presumably was prompted by the overflow of reserve capacity reported in this blog's October post. The team's recommendations included getting accurate statistics to find out how much cotton production is actually produced; adjusting the structure of products transported, "improving rail work"; and exploring ways of storing cotton in courtyards, finding more space in warehouses and using them more efficiently.

Agricultural officials worry that Chinese farmers will abandon cotton production in droves if the cotton price declines. A team of Ministry of Agriculture analysts visited several cotton-producing counties in eastern China during October. They found that cotton yields were good this year and net returns from planting cotton were up 30 percent from 2011. However, farmers in this region can make more from planting winter wheat followed by a summer corn crop. Also, cotton takes a lot more labor, a problem for farmers who can earn a lot more working off-farm. Officials in the regions they visited expected more declines in cotton production next year.

The team of agriculture analysts recommended extending the "general input subsidy" to cotton farmers--this subsidy is now given only to grain producers. They called for beginning the general input subsidy for cotton in Xinjiang next year and later spreading it to other provinces. (The only direct subsidy for cotton producers now is 15 yuan per mu for improved seed varieties.) In Xinjiang (and Shandong) the general input subsidy for grain is distributed based on the area planted in wheat, so adding a subsidy for cotton would be seemingly straightforward. However, in Hebei and Henan Provinces (also big cotton-producing areas) the general input subsidy is now a decoupled payment based on a farmer's historical land parcel designated for producing grain, but there is no formal requirement that they plant grain. In these provinces, farmers may already be planting cotton on part of this land, so it would be problematic to implement a general input subsidy for cotton.

The agricultural analysts also called for announcing the support price as early as possible--before they plant the crop in the spring--to give farmers "confidence" and incentives to produce.

There is no discussion of how China will dispose of its massive cotton stockpile. The Ministry of Agriculture analysts make some vague recommendations in this direction. They call for adjusting the annual import quota based on international and domestic market conditions and using other inducements to encourage companies to use Chinese cotton. These proposals sound like WTO violations, however, and Ministry of Agriculture officials regularly insist that they adhere to their WTO commitments.

For now, Chinese authorities are subsidizing domestic producers by stockpiling their cotton at artificially-high prices, and they are subsidizing cotton producers in the United States, Australia, India and elsewhere overseas by creating an artificially-high demand for cotton as they lock up half the Chinese crop in warehouses. Chinese officials may be hoping there will be a rebound in textile demand that will allow them to sell off the reserves at a price higher than they paid. Some reserves from last year are being sold to textile companies at last year's price now. It would take a lot of demand to use up the volume they have accumulated.

Finally, as with most buffer stock policies, the result is the opposite of what was intended. The idea of the price support was to stabilize the cotton market, but instead it has created even more confusion and potential instability. Chinese cotton production continues to fall; the subsidy cost soars. In the same way Chinese businesses copy factories and products overseas, Chinese officials adopt policies discovered in textbooks or overseas study tours without carefully thinking through the potential outcomes.

Unlike the E.U. and U.S. price support regimes of earlier decades, China has committed to relatively low tariffs and China is a net importer of cotton. The E.U. and U.S. subsidized exports of their commodity mountains, distorting world markets and leading to the adoption of disciplines on domestic support in the Uruguay Round of GATT. China, however, is accumulating a mountain of domestic cotton AND importing huge quantities of cotton. This is the perverse three-tier market described on this blog in October.

As of December 5, China's national cotton reserve corporation had purchased a cumulative 3.6 million metric tons of cotton from the 2012 harvest. This is the second year of massive stockpiling after the price support policy was introduced in 2011. The addition to the stockpile from this harvest so far exceeds the addition to last year's stockpile of about 3.1 mmt. Total reserves are now near 7.5 million metric tons. This exceeds China's annual production--estimated at 6.6 mmt this year--and is about 75 percent of USDA's estimate of China's annual consumption of cotton.

The cotton mountain phenomenon is exacerbated by weak demand for cotton from the Chinese textile industry. The textile business in China is still relatively slow. There are signs of recovery in domestic apparel sales but the export business is not good. Many companies report very slow orders.

For the most part, the only buyers of cotton in the China market now are companies that are authorized to buy at the minimum price. Private-sector operators are only buying cotton as they need it. Many companies in the textile business have either idled their factories or are running at a fraction of capacity. Those still operating are losing money and continue operating either to keep workers busy or to fulfill orders for high-end products. Inventories of unsold textiles are up. Companies are reportedly facing cash flow pressure. They have to repay outstanding loans before getting new ones. Many are having trouble paying their employees. Reportedly, more textile operators will have to shut down around the new year.

Imported cotton is cheaper than domestic cotton at the support price, so companies looking for cotton try to get imports. Cotton imports are controlled by a tariff rate quota system installed after WTO accession. According to a cotton industry report, quotas to import have become a valuable right. Some trading companies holding quotas import cheap cotton and resell it to Chinese companies at a price near the support price. Some textile industry people say the availability of cotton imported at the 40 percent sliding scale tariff has recently been restricted by some unspecified policies.

China's imports of cotton soared to 5.4 mmt during 2011/12, more than double imports of about 2.5 mmt during the previous two years. According to Chinese customs statistics, imports during the first two months of the 2012/13 market year are at about the same pace as last year.

Why did China pursue this policy? According to Ministry of Agriculture surveys, farmers wanted a price support policy. Ministry economists explained in a 2011 report that the policy was meant to address "cobweb"-type oscillations in the cotton market--a low price induces a decline in production which leads to high prices the following year, which leads to expanding production, which leads to low prices... Previously, the government tried to manage reserves to stabilize the cotton market, but it didn't have much impact and farmers didn't perceive any benefit from the policy.

An unspoken strategy behind the cotton policy is to buy regional stability in China's restive northwest Xinjiang "autonomous" region. Chinese authorities built up a cotton industry in Xinjiang during the 1990s to maintain self-sufficiency as cotton use swelled and eastern production areas faced pest problems. Xinjiang now accounts for nearly half of China's cotton production and would be one of the top producers in the world if it were a country. About two-thirds of the reserve purchases under the price support program are made in Xinjiang.

Xinjiang borders several central Asian countries and was the site of violent protests by the native Uighur population in 2009 and 2011. China's President Hu Jintao recently noted that policies are tilted toward border regions (check) and ethnic minority regions (check). A Ministry of Agriculture article offering recommendations for the design of the policy noted the importance of supporting poor farmers in Xinjiang who, unlike farmers in eastern China, had no good alternatives to growing cotton.

The problem with creating a cotton industry in Xinjiang is that it's thousands of miles from the textile industry and there has been very little progress in developing a local industry beyond basic cotton-ginning and trading. On December 7, a team of officials from the National Development and Reform Commission, Railway Ministry, Supply and Market Cooperative and National Cotton Reserve Corporation went to Xinjiang to inspect the situation regarding purchase, reserves and transportation of cotton. This presumably was prompted by the overflow of reserve capacity reported in this blog's October post. The team's recommendations included getting accurate statistics to find out how much cotton production is actually produced; adjusting the structure of products transported, "improving rail work"; and exploring ways of storing cotton in courtyards, finding more space in warehouses and using them more efficiently.

Agricultural officials worry that Chinese farmers will abandon cotton production in droves if the cotton price declines. A team of Ministry of Agriculture analysts visited several cotton-producing counties in eastern China during October. They found that cotton yields were good this year and net returns from planting cotton were up 30 percent from 2011. However, farmers in this region can make more from planting winter wheat followed by a summer corn crop. Also, cotton takes a lot more labor, a problem for farmers who can earn a lot more working off-farm. Officials in the regions they visited expected more declines in cotton production next year.

The team of agriculture analysts recommended extending the "general input subsidy" to cotton farmers--this subsidy is now given only to grain producers. They called for beginning the general input subsidy for cotton in Xinjiang next year and later spreading it to other provinces. (The only direct subsidy for cotton producers now is 15 yuan per mu for improved seed varieties.) In Xinjiang (and Shandong) the general input subsidy for grain is distributed based on the area planted in wheat, so adding a subsidy for cotton would be seemingly straightforward. However, in Hebei and Henan Provinces (also big cotton-producing areas) the general input subsidy is now a decoupled payment based on a farmer's historical land parcel designated for producing grain, but there is no formal requirement that they plant grain. In these provinces, farmers may already be planting cotton on part of this land, so it would be problematic to implement a general input subsidy for cotton.

The agricultural analysts also called for announcing the support price as early as possible--before they plant the crop in the spring--to give farmers "confidence" and incentives to produce.

There is no discussion of how China will dispose of its massive cotton stockpile. The Ministry of Agriculture analysts make some vague recommendations in this direction. They call for adjusting the annual import quota based on international and domestic market conditions and using other inducements to encourage companies to use Chinese cotton. These proposals sound like WTO violations, however, and Ministry of Agriculture officials regularly insist that they adhere to their WTO commitments.

For now, Chinese authorities are subsidizing domestic producers by stockpiling their cotton at artificially-high prices, and they are subsidizing cotton producers in the United States, Australia, India and elsewhere overseas by creating an artificially-high demand for cotton as they lock up half the Chinese crop in warehouses. Chinese officials may be hoping there will be a rebound in textile demand that will allow them to sell off the reserves at a price higher than they paid. Some reserves from last year are being sold to textile companies at last year's price now. It would take a lot of demand to use up the volume they have accumulated.

Finally, as with most buffer stock policies, the result is the opposite of what was intended. The idea of the price support was to stabilize the cotton market, but instead it has created even more confusion and potential instability. Chinese cotton production continues to fall; the subsidy cost soars. In the same way Chinese businesses copy factories and products overseas, Chinese officials adopt policies discovered in textbooks or overseas study tours without carefully thinking through the potential outcomes.

Farming Structure Change Encouraged in 2013

The "Number 1 Document" will emphasize a transition to larger-scale farms next year, according to a reporter's posting on the Economy Reference News microblog.

The document will call for rural households to remain the primary operators of farms while encouraging innovations in arrangements that create large individual-operated farms, family farms, cooperatives, and contracting relationships between farmers and companies. However, commercial enterprises will be discouraged from renting large tracts of land from rural households or renting on a long-term basis in order to prevent them from converting land to non-grain or non-agricultural uses.

The campaign for new farming arrangements is motivated by the massive outmigration of rural laborers, aging rural population, the emerging dominance of part-time farming and the conundrum of "who will farm"? Against this background, fostering new-style farms has become more "urgent."

This is not a new strategy. A document on rural strategy issued by the third plenum of the 17th Party Congress in 2008 encouraged such explorations. Since then many local governments have been experimenting with setting up land rental markets and giving subsidies to large farms and awards for consolidating plots of land. Look for these to become national policies next year.

Don't plan on investing in Chinese farmland. At a meeting of the standing committee of the State Council this week it was pronounced that rural households are not only the appropriate operators in a fragmented small-farm system, but also appropriate as the main operators of commercial-scale farms. At an agricultural work meeting, Minister of Agriculture Han Changfu said commercial enterprises are welcome to invest in agriculture but they are not encouraged to enter into long-term land rentals.

Han said that 20 percent of rural land has been transferred (up from about 4 percent in the mid-2000s) and commercial-scale operation of farms has increased. He said that small-scale and larger-scale farms will coexist for a long time, presumably an assurance that farmers will not be forced off their land. Han said consolidation of land must be coordinated with rural peoples' employment, migration and urbanization. Companies, he said, must "pull along" rural people, not replace them as producers.

The document will call for rural households to remain the primary operators of farms while encouraging innovations in arrangements that create large individual-operated farms, family farms, cooperatives, and contracting relationships between farmers and companies. However, commercial enterprises will be discouraged from renting large tracts of land from rural households or renting on a long-term basis in order to prevent them from converting land to non-grain or non-agricultural uses.

The campaign for new farming arrangements is motivated by the massive outmigration of rural laborers, aging rural population, the emerging dominance of part-time farming and the conundrum of "who will farm"? Against this background, fostering new-style farms has become more "urgent."

This is not a new strategy. A document on rural strategy issued by the third plenum of the 17th Party Congress in 2008 encouraged such explorations. Since then many local governments have been experimenting with setting up land rental markets and giving subsidies to large farms and awards for consolidating plots of land. Look for these to become national policies next year.

Don't plan on investing in Chinese farmland. At a meeting of the standing committee of the State Council this week it was pronounced that rural households are not only the appropriate operators in a fragmented small-farm system, but also appropriate as the main operators of commercial-scale farms. At an agricultural work meeting, Minister of Agriculture Han Changfu said commercial enterprises are welcome to invest in agriculture but they are not encouraged to enter into long-term land rentals.

Han said that 20 percent of rural land has been transferred (up from about 4 percent in the mid-2000s) and commercial-scale operation of farms has increased. He said that small-scale and larger-scale farms will coexist for a long time, presumably an assurance that farmers will not be forced off their land. Han said consolidation of land must be coordinated with rural peoples' employment, migration and urbanization. Companies, he said, must "pull along" rural people, not replace them as producers.

Chinese City Imports Rice From 7 Countries

In another sign of China's transition from a country of farmers to a consumer country, a city in Fujian Province is importing rice from seven countries this year to keep a lid on prices.

Xiamen is a prosperous port just across the straight from Taiwan. This year local grain companies have struck deals with Thailand, Vietnam, Pakistan, Uruguay, Burma, Cambodia and India to supply rice to the local market. Xiamen has imported 100,000 metric tons of rice in the first ten months of this year. There are four new countries supplying imports this year and India will begin exporting to Xiamen after procedures are completed.

A representative from a local grain company explained that Xiamen relies on bringing in rice from elsewhere since it doesn't have a lot of local production. The purpose of the imports is to satisfy local demand and keep prices down. The imported rice from Vietnam and Pakistan costs about 2 yuan per 500g, about 40 percent less than Thai rice.

The article says that in the fourth quarter of this year the government will eliminate quarantine and inspection fees on imported rice. This will reduce the cost to companies by 28 percent.

The imported rice, however, is kept segregated from the general market to minimize competition with domestic rice. It can't be sold directly in retail markets. According to the article, regulations prohibit the imported rice from being sold under a brand name in order "to protect local companies."

Rice mill managers say local consumers are not accustomed to the taste of the Vietnamese and Pakistani rice and none of the supermarkets sell it. They say the imported rice is mainly used for food processing or in cafeterias for factory workers. Some mills mix it with domestic rice. A manager remarks that the rice from Uruguay is not bad. Ironically, it is often sold to "western restaurants" to be used for fried rice.

A Xiamen grain bureau official credits the imported rice for keeping prices down despite rising prices in production areas recently. A local grain company official remarked that some of the imported rice is transported to inland areas where it puts downward pressure on rice prices.

Xiamen is a prosperous port just across the straight from Taiwan. This year local grain companies have struck deals with Thailand, Vietnam, Pakistan, Uruguay, Burma, Cambodia and India to supply rice to the local market. Xiamen has imported 100,000 metric tons of rice in the first ten months of this year. There are four new countries supplying imports this year and India will begin exporting to Xiamen after procedures are completed.

A representative from a local grain company explained that Xiamen relies on bringing in rice from elsewhere since it doesn't have a lot of local production. The purpose of the imports is to satisfy local demand and keep prices down. The imported rice from Vietnam and Pakistan costs about 2 yuan per 500g, about 40 percent less than Thai rice.

The article says that in the fourth quarter of this year the government will eliminate quarantine and inspection fees on imported rice. This will reduce the cost to companies by 28 percent.

The imported rice, however, is kept segregated from the general market to minimize competition with domestic rice. It can't be sold directly in retail markets. According to the article, regulations prohibit the imported rice from being sold under a brand name in order "to protect local companies."

Rice mill managers say local consumers are not accustomed to the taste of the Vietnamese and Pakistani rice and none of the supermarkets sell it. They say the imported rice is mainly used for food processing or in cafeterias for factory workers. Some mills mix it with domestic rice. A manager remarks that the rice from Uruguay is not bad. Ironically, it is often sold to "western restaurants" to be used for fried rice.

A Xiamen grain bureau official credits the imported rice for keeping prices down despite rising prices in production areas recently. A local grain company official remarked that some of the imported rice is transported to inland areas where it puts downward pressure on rice prices.

Time to Abandon the Food Self-Sufficiency Delusion?

An opinion piece circulating on China's Internet calls for China to give up its near-sacred goal of self-sufficiency in grain.

For a long time Chinese government officials have stressed the importance of maintaining self-sufficiency in grain with rhetoric like, "The Chinese peoples' rice bowl must be firmly in their own hands." The 2008 medium and long-term plan for food security insisted that China must produce at least 95 percent of the grain it consumes. The Ministry of Agriculture reiterated the self-sufficiency goal in February of this year.

The article places the self-sufficiency issue in historical context. It suggests that the insistence on self-sufficiency is based on China's history as an agricultural country with a large population. It refers to the huge famine in the early 1960s, referring to it as a "manmade disaster" (officials still refer to it as several years of "natural disaster"), as an event that influences the grain self-sufficiency fixation.

The article picks up on the "urbanization" mantra that dominates official rhetoric about China's new stage of historical development. While not stated explicitly, the article seems to imply that China should quit pretending it can remain a big agricultural country that feeds itself as it becomes an urbanized society. With China facing a huge task of urbanization, cities will have to expand, reducing land available for agriculture, argues the article's author. China should be realistic and prepare to become the world's biggest importer of agricultural products.

The writer quotes Chen Xiwen, the country's top rural policy advisor, who has acknowledged that China would need 3 billion mu of land planted in crops to eliminate agricultral imports, but it only has 2.4 billion mu--a deficit of 20 percent. The article also cites an assertion by the Chinese Academy of Social Sciences that China's cultivated land area has already dipped below the 1.8-billion-mu "red line" deemed necessary for maintaining food security. (The 1.8 billion mu refers to the physical amount of land available; the 2.4 billion presumably double-counts land that has two crops a year planted on it.)

The NBS announced this month that grain production increased in 2012 for the ninth year in a row. The total grain output of 589 million metric tons this year already exceeded the goal of 550 mmt for 2020. Yet China already imported over 60 mmt of grains and soybeans in the first ten months of this year. Since last year China has been a net importer of all the major grain crops--corn, wheat and even rice. The article says grain and soybean imports are on track to reach 72 mmt this year, which would be 10.9 percent of all grain consumed in China.

The article warns that it is inevitable that China will become a bigger importer of grain. It already accounts for 30 percent of world trade. China needs to pay attention to overseas trends and developments. China must be more proactive, buy or rent land overseas, invest in foreign agricultural and trading companies, and gain influence and control in world agricultural markets, argues the author.

The writer recommends that grain prices be increased. This would make agriculture more profitable and attract capital investment needed to upgrade the agricultural industry. China needs to reverse its traditional "scissors policy" of setting low prices for agricultural commodities to subsidize industry and urbanization.

For a long time Chinese government officials have stressed the importance of maintaining self-sufficiency in grain with rhetoric like, "The Chinese peoples' rice bowl must be firmly in their own hands." The 2008 medium and long-term plan for food security insisted that China must produce at least 95 percent of the grain it consumes. The Ministry of Agriculture reiterated the self-sufficiency goal in February of this year.

The article places the self-sufficiency issue in historical context. It suggests that the insistence on self-sufficiency is based on China's history as an agricultural country with a large population. It refers to the huge famine in the early 1960s, referring to it as a "manmade disaster" (officials still refer to it as several years of "natural disaster"), as an event that influences the grain self-sufficiency fixation.

The article picks up on the "urbanization" mantra that dominates official rhetoric about China's new stage of historical development. While not stated explicitly, the article seems to imply that China should quit pretending it can remain a big agricultural country that feeds itself as it becomes an urbanized society. With China facing a huge task of urbanization, cities will have to expand, reducing land available for agriculture, argues the article's author. China should be realistic and prepare to become the world's biggest importer of agricultural products.

The writer quotes Chen Xiwen, the country's top rural policy advisor, who has acknowledged that China would need 3 billion mu of land planted in crops to eliminate agricultral imports, but it only has 2.4 billion mu--a deficit of 20 percent. The article also cites an assertion by the Chinese Academy of Social Sciences that China's cultivated land area has already dipped below the 1.8-billion-mu "red line" deemed necessary for maintaining food security. (The 1.8 billion mu refers to the physical amount of land available; the 2.4 billion presumably double-counts land that has two crops a year planted on it.)

The NBS announced this month that grain production increased in 2012 for the ninth year in a row. The total grain output of 589 million metric tons this year already exceeded the goal of 550 mmt for 2020. Yet China already imported over 60 mmt of grains and soybeans in the first ten months of this year. Since last year China has been a net importer of all the major grain crops--corn, wheat and even rice. The article says grain and soybean imports are on track to reach 72 mmt this year, which would be 10.9 percent of all grain consumed in China.

The article warns that it is inevitable that China will become a bigger importer of grain. It already accounts for 30 percent of world trade. China needs to pay attention to overseas trends and developments. China must be more proactive, buy or rent land overseas, invest in foreign agricultural and trading companies, and gain influence and control in world agricultural markets, argues the author.

The writer recommends that grain prices be increased. This would make agriculture more profitable and attract capital investment needed to upgrade the agricultural industry. China needs to reverse its traditional "scissors policy" of setting low prices for agricultural commodities to subsidize industry and urbanization.

China 2012 Grain Production Statistics Released

China had another abundant grain harvest in 2012 that exceeded 589 million metric tons (mmt) according to estimates from the National Bureau of Statistics (NBS) released November 30. NBS estimates that production rose 3.2 percent during 2012, an increase they attribute to good weather and policies. The statistics are shown in a table below.

Somehow, Chinese farmers found 694,000 hectares of land to expand the area planted in grain. Grain area increased by 0.6 percent and yield increased by 4.1 percent. NBS estimated that increases in yields contributed 14.78 mmt of additional grain output while expanded plantings contributed 3.58 mmt.

A major development highlighted by the statistics is the emergence of corn as China's biggest crop in both area and output. Corn production is estimated at 208 mmt, surpassing rice output (204 mmt) for the first time. The increase in corn output came mainly from increase in area. Corn area rose 4.2 percent and yield grew 3.6 percent. Rice area and yields both grew less than 1 percent. Wheat area was down but NBS says yield was up 3.3 percent.

The net growth in grain area reflects a big expansion of corn planting to meet the growing demand for feed, starches, alcohol and sweeteners made from corn. Corn planting increased by 1.4 million hectares (4.2-percent). Where did farmers find land to plant more corn? Some of it came from switching from soybeans to corn. NBS reports a decrease of 712,000 hectares (9 percent) in soybean plantings. However, the decrease in soybean area accounts for--at most--only half of the increase in corn area. Some area might have come from minor grains like millet, sorghum and mung beans, but the NBS numbers imply a decrease in area for these other grains of only 110,000 hectares.

NBS said the improvement in crop yields reflected good weather, including plentiful rainfall, adequate sunshine and higher temperatures than usual. There is no mention of typhoons, leaf hoppers, wheat fungus, corn borers or army worms.

The report begins by citing the strong support for grain production from the central committee of the communist party and the state council for the increase in grain output. It specifically cites a set of programs described as disaster mitigation strategies. These include an expansion of specialized pest control teams and a "three preventions with one spray" program for wheat. When insects showed up, teams were organized to drench the fields with pesticides. There is also a campaign to grow rice seedlings under plastic tunnels in the northeast, and a "sit in water" strategy. In south China there was a big campaign this year to subsidize farms that specialize in propagating seedlings for the early rice crop. Another campaign to address the chronic drought in southwestern provinces promoted the use of plastic mulch to retain moisture in the soil for growing corn.

The report cites the government's four major subsidies (a direct payment, general input subsidy, seed subsidy and machinery purchase subsidy) for supporting grain production. NBS also gives credit to price support programs for sending a strong signal to encourage grain production by early announcement of prices (i.e. before planting). The report doesn't mention it, but many provinces expanded their subsidies to over 100 yuan per mu this year and some are linking the subsidies more closely to area planted. There was an additional "general input subsidy" that amounted to about 20 yuan per mu to compensate farmers for the government's increase in fuel prices. In Shandong Province subsidies were raised to 120 yuan this year with a 10-yuan bonus for farms of 100 mu or larger, and officials there began using remote sensing satellite imagery to verify subsidized wheat area.

Somehow, Chinese farmers found 694,000 hectares of land to expand the area planted in grain. Grain area increased by 0.6 percent and yield increased by 4.1 percent. NBS estimated that increases in yields contributed 14.78 mmt of additional grain output while expanded plantings contributed 3.58 mmt.

A major development highlighted by the statistics is the emergence of corn as China's biggest crop in both area and output. Corn production is estimated at 208 mmt, surpassing rice output (204 mmt) for the first time. The increase in corn output came mainly from increase in area. Corn area rose 4.2 percent and yield grew 3.6 percent. Rice area and yields both grew less than 1 percent. Wheat area was down but NBS says yield was up 3.3 percent.

The net growth in grain area reflects a big expansion of corn planting to meet the growing demand for feed, starches, alcohol and sweeteners made from corn. Corn planting increased by 1.4 million hectares (4.2-percent). Where did farmers find land to plant more corn? Some of it came from switching from soybeans to corn. NBS reports a decrease of 712,000 hectares (9 percent) in soybean plantings. However, the decrease in soybean area accounts for--at most--only half of the increase in corn area. Some area might have come from minor grains like millet, sorghum and mung beans, but the NBS numbers imply a decrease in area for these other grains of only 110,000 hectares.

NBS said the improvement in crop yields reflected good weather, including plentiful rainfall, adequate sunshine and higher temperatures than usual. There is no mention of typhoons, leaf hoppers, wheat fungus, corn borers or army worms.

The report begins by citing the strong support for grain production from the central committee of the communist party and the state council for the increase in grain output. It specifically cites a set of programs described as disaster mitigation strategies. These include an expansion of specialized pest control teams and a "three preventions with one spray" program for wheat. When insects showed up, teams were organized to drench the fields with pesticides. There is also a campaign to grow rice seedlings under plastic tunnels in the northeast, and a "sit in water" strategy. In south China there was a big campaign this year to subsidize farms that specialize in propagating seedlings for the early rice crop. Another campaign to address the chronic drought in southwestern provinces promoted the use of plastic mulch to retain moisture in the soil for growing corn.